Stop Paying for Fires and Floods. Start Preventing Them.

Partner with FireBot to shift from a reactive "Repair and Replace" model to a proactive "Predict and Prevent" paradigm. Deploy our UL 300A-tested smart fire and water protection systems across your policyholder base to slash claim frequency, reduce payout severity, and unlock unprecedented data for the next generation of underwriting.

Become an Insurance Partner

"*" indicates required fields

The Two-Headed Dragon Costing You Billions

The Stovetop Fire Epidemic

Nearly 50% of all home fires start on the stovetop, leading to 175,000 incidents and over $8.4 billion in property damage annually in the U.S.. Unattended cooking remains the primary cause.

The Constant Threat of Water Damage

Water damage is the most common home insurance claim, affecting 14,000 Americans daily. The average claim now exceeds $12,500, costing the industry billions each year from predictable causes like burst pipes and appliance failures.

Our Proactive Protection Ecosystem

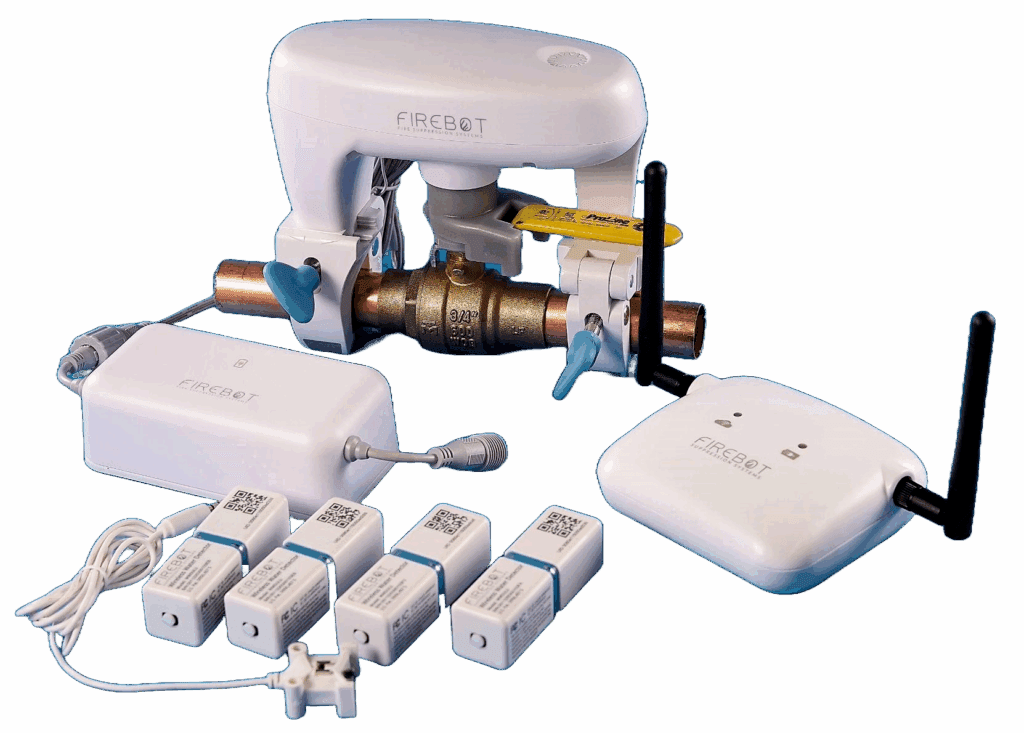

The FireBot Stovetop Fire Suppression System

Intelligent, Automatic Suppression

Smart thermal sensors differentiate between normal cooking heat and a dangerous flare-up. Before a fire can spread, FireBot automatically deploys a non-toxic, biodegradable liquid agent that extinguishes the flames, cools hot surfaces to prevent re-ignition, and is simple to clean up.

The Gold Standard of Safety

UL 300A Tested:FireBot is the only device in its class tested by a Nationally Recognized Testing Laboratory (NRTL) to meet the rigorous UL 300A standard for residential cooktop fire suppression. This is the same benchmark used for commercial kitchens, providing objective, third-party proof of performance that you and your policyholders can trust. As an insurer, you know you cannot endorse a life-safety product that lacks a UL rating.

The FireBot Stovetop Fire Suppression System

Intelligent, Automatic Suppression

Smart thermal sensors differentiate between normal cooking heat and a dangerous flare-up. Before a fire can spread, FireBot automatically deploys a non-toxic, biodegradable liquid agent that extinguishes the flames, cools hot surfaces to prevent re-ignition, and is simple to clean up.

The Gold Standard of Safety

UL 300A Tested:FireBot is the only device in its class tested by a Nationally Recognized Testing Laboratory (NRTL) to meet the rigorous UL 300A standard for residential cooktop fire suppression. This is the same benchmark used for commercial kitchens, providing objective, third-party proof of performance that you and your policyholders can trust. As an insurer, you know you cannot endorse a life-safety product that lacks a UL rating.

The FireBot Water Damage Prevention System

Reliable, Long-Range Detection

Our wireless leak detectors feature a 10-year battery life and use robust LoRa communication, ensuring they work even during power or internet outages—a critical feature for reliable protection. They detect both leaks and freeze conditions that lead to burst pipes.

Automated Water Shutoff

When a leak is detected, the system instantly signals our revolutionary Ball Valve Servo (BVS) Water Shutoff. This device is a game-changer for scalability; it’s a retrofit actuator that installs over the existing main water valve in minutes without a plumber or cutting pipes. It immediately stops the flow of water, preventing a potential disaster.

Why FireBot is the Superior Risk Mitigation Tool

| Technology | FireBot Suppression System | Traditional Sprinkler System | Dry Powder Suppressors | Standard Smoke Alarm |

|---|---|---|---|---|

| Primary Function | Active Suppression | Active Suppression | Active Suppression | Passive Alert |

| Claim Impact | Prevents fire claim AND secondary water damage claim. FireBot activates before sprinklers, using only 1 liter of clean, non-toxic liquid. | Often causes a water damage claim far more expensive than the initial fire damage it was meant to stop. | Suppresses fire but creates a massive, corrosive mess, leading to extensive cleanup and replacement costs. | Alerts only after a fire has started and damage is underway. Does not prevent the loss. |

| Activation Method | Smart thermal sensors detect dangerous heat patterns, preventing false alarms from smoke. | High heat triggers a system-wide water release. | A physical fuse must be engulfed in flame, resulting in a delayed reaction. | Detects smoke particles, leading to frequent false alarms from cooking. |

| Safety Standard | Tested to UL 300A, the commercial-grade standard for residential cooktops. | N/A for stovetop specificity. | Not UL 300A compliant. | UL 217 (Standard for Smoke Alarms). |

| Policyholder Value | Peace of mind with a smart, clean, and effective system that actively protects their home. | Fear of accidental activation and catastrophic water damage. | A low-cost but messy and potentially damaging solution. | A basic, required safety measure. |

FireBot Suppression System

Primary Function

Active Suppression

Claim Impact

Prevents fire claim AND secondary water damage claim. FireBot activates before sprinklers, using only 1 liter of clean, non-toxic liquid.

Activation Method

Smart thermal sensors detect dangerous heat patterns, preventing false alarms from smoke.

Safety Standard

Tested to UL 300A, the commercial-grade standard for residential cooktops.

Policyholder Value

Peace of mind with a smart, clean, and effective system that actively protects their home.

Traditional Sprinkler System

Primary Function

Active Suppression

Claim Impact

Often causes a water damage claim far more expensive than the initial fire damage it was meant to stop.

Activation Method

High heat triggers a system-wide water release.

Safety Standard

N/A for stovetop specificity.

Policyholder Value

Fear of accidental activation and catastrophic water damage.

Dry Powder Suppressors

Primary Function

Active Suppression

Claim Impact

Suppresses fire but creates a massive, corrosive mess, leading to extensive cleanup and replacement costs.

Activation Method

A physical fuse must be engulfed in flame, resulting in a delayed reaction.

Safety Standard

Not UL 300A compliant.

Policyholder Value

A low-cost but messy and potentially damaging solution.

Standard Smoke Alarm

Primary Function

Passive Alert

Claim Impact

Alerts only after a fire has started and damage is underway. Does not prevent the loss.

Activation Method

Detects smoke particles, leading to frequent false alarms from cooking.

Safety Standard

UL 217 (Standard for Smoke Alarms).

Policyholder Value

A basic, required safety measure.

FireBot is the only solution that intelligently stops the #1 cause of home fires with surgical precision, protecting the property without inflicting costly collateral damage.

Our Proactive Protection Ecosystem

The FireBot Water Damage Prevention System

Reliable, Long-Range Detection

Our wireless leak detectors feature a 10-year battery life and use robust LoRa communication, ensuring they work even during power or internet outages—a critical feature for reliable protection. They detect both leaks and freeze conditions that lead to burst pipes.

Automated Water Shutoff

When a leak is detected, the system instantly signals our revolutionary Ball Valve Servo (BVS) Water Shutoff. This device is a game-changer for scalability; it’s a retrofit actuator that installs over the existing main water valve in minutes without a plumber or cutting pipes. It immediately stops the flow of water, preventing a potential disaster.

The Next Seatbelt Moment: Leading the Shift to Active Protection

A Familiar Resistance to a Revolutionary Idea

When seatbelts were first introduced, the reaction was not universal acceptance. Despite a federal law in 1968 requiring them to be installed in all new cars, usage rates remained below 15% for years. The debate was fierce, often pitting arguments of personal freedom against the clear data on public safety. It took a powerful coalition of government regulators, public awareness campaigns, and pressure from the auto and insurance industries to drive the cultural shift. That concerted effort is why seatbelt use now exceeds 90% and saves an estimated 15,000 lives every year.

Today's Home is in the "Pre-Mandate" Era

The parallel to home safety is striking. A standard smoke alarm is the equivalent of a car with seatbelts that are never buckled. It is a passive device that can only alert you to a disaster already in progress, doing nothing to prevent the catastrophic outcome.

FireBot is the act of buckling up. It is the crucial, proactive step that intervenes to prevent the loss. Our UL 300A-tested fire suppression system and automatic water shutoff valve don’t just warn of danger—they actively stop it.

Your Role as the Catalyst for Change

Just as the insurance industry was a key player in advocating for seatbelt use to reduce catastrophic losses, today’s insurers are in the unique position to champion this new standard of home safety. By creating strong financial incentives—significant premium discounts—for the adoption of active protection systems like FireBot, you are not just offering a new discount category. You are leading a public safety revolution. The result is the same: billions saved in claims, a more resilient housing stock, and most importantly, lives protected.

Partner with us to lead this change and make every home a "buckled-up" home!

A Partnership Built for Seamless Integration

We understand that a successful program requires more than just great technology. It requires a frictionless rollout for you and your policyholders. Our partnership model is designed for simplicity and scale.

Effortless Policyholder Adoption

No plumbers or electricians are required

Flexible and Scalable Programs

Co-Branded Marketing & Support

Dedicated Partner Success Team

The Future of Underwriting is Here: Unlock In-Home IoT Data

Hyper-Personalized Underwriting

Stop relying on static demographic data. With anonymized, aggregated data from FireBot devices, you can develop dynamic, usage-based insurance (UBI) models for the home, pricing risk with unprecedented accuracy.

Proactive Risk Mitigation

Our system provides early warnings for potential claims. Get alerts on freezing pipe conditions, low device batteries, or other anomalies, allowing you to engage with policyholders and prevent a loss before it happens.

Streamlined & Fraud-Proof Claims

n the event of a claim, IoT data provides an objective, time-stamped record of the incident. This accelerates the validation process, improves payout accuracy, and helps detect fraudulent activity, potentially cutting claims processing costs by up to 30%.

Become a FireBot Insurance Partner in 3 Simple Steps

We make it easy to integrate our proactive protection solutions into your offerings.

Consultation

Schedule a meeting with our partnership team to discuss your goals and how FireBot can align with your strategic objectives.

Program Design

We’ll work with you to create a custom rollout plan, from pilot programs to full policyholder integration, including co-branded marketing materials.

Launch & Save

Deploy the program to your policyholders and start seeing the immediate benefits of reduced claims, increased loyalty, and a smarter risk portfolio.